FAQ on Liberalisation of Motor Insurance

1. What does the liberalisation of motor insurance mean?

The liberalisation of motor insurance means that the price of motor insurance products will no longer be determined based on Motor Tariff (a set fixed price list). Pricing will be determined by individual insurers and takaful operators.

Consumers will now be able to enjoy a wider choice of motor insurance products at competitive prices as liberalisation encourages innovation and competition among insurers and takaful operators.

Insurers and takaful operators are able to charge premiums that are in line with broader risk factors inherent in a group of policyholders being insured; and also sell new products that are not defined under the tariff.

2. How is insurance premium calculated today?

Insurance premium is calculated based on the sum insured and model of the vehicle. Additionally, insurers are allowed to apply limited premium loading based on the age of the driver and the number of accidents on record. Depending on the driver’s claims history, the calculated premium to be paid is adjusted against the

discount (No Claim Discount or NCD).

Typically, drivers with good driving records can enjoy a higher percentage of NCD up to 55%.

However, the driver may experience receiving different quotes from different insurers due to other factors mentioned above.

3. How will insurance premiums be priced from 1 July 2017 onwards?

Effective 1 July 2017, under the liberalised environment, more risk factors will be taken into account in

determining premiums. Other than the sum insured, cubic capacity of the vehicle engine, age of vehicle and age of driver, premiums may be driven by other factors. These factors could be safety and security features in the vehicle, duration that the vehicle is on the road, geographical location of the vehicle (in areas with higher incidents of theft) and traffic offences on record. These factors will define the risk profile group of the policyholder which will determine the premium.

As different insurers and takaful operators have different ways of defining the risk profile group, the price of a motor policy would differ from one insurer to another.

4. When will the Liberalisation of Motor Tariffs be implemented?

The first phase of the Liberalisation of the Motor and Fire Tariff was introduced on 1 July 2016. During this initial phase, insurers and takaful operators were given the flexibility to offer new motor products and add-on covers that were not defined under the existing tariff.

From 1 July 2017 onwards, premium rates for Motor Comprehensive; and Motor Third Party Fire and Theft products will be liberalised where premium pricing will be determined by individual insurers and takaful operators.

However, premium rates for Motor Third Party product will continue to be subjected to tariff rates.

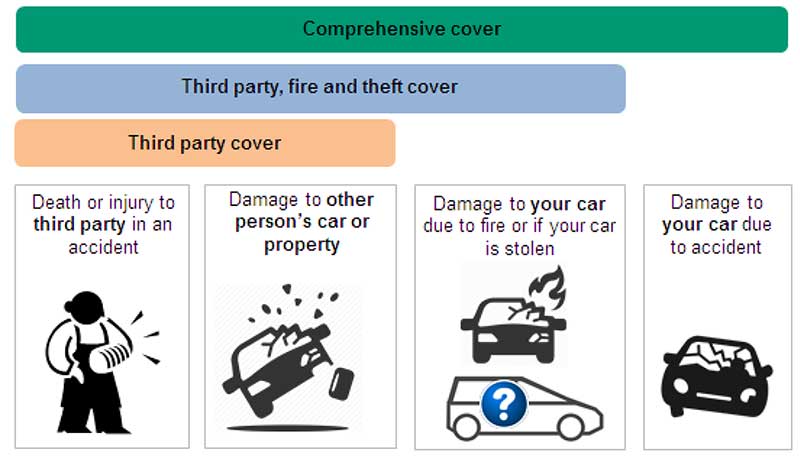

The existing motor products and coverage are:

5. What are the benefits of the Liberalisation of Motor Tariffs?

For consumers, the benefits include:

- An improvement in the quality of service and a wider range of products at competitive prices due to greater competition among insurers;

- The availability of new products with different features that will enable consumers and businesses to obtain the coverage that best meets their insurance needs;

- As safety features will be one of the factors to determine premiums, drivers will be incentivised to inculcate safe driving habits which will benefit them and the general public.

- Competitive pricing will be offered by insurers and takaful operators where consumers may benefit from shopping around to obtain the best deals that suit their needs.

- New distribution channels such as cost efficient online channels would enable insurance protection to be purchased in a manner most convenient to consumers.

6.What should I do when buying my insurance cover in a liberalised market?

Consumers should consider the following points when buying insurance:

- You should not be looking at pricing as the only factor when purchasing motor insurance protection plan. You should also look for what the policy covers, exclusions and customer service standards.

- You should shop around by contacting the agents, insurers or takaful operators through their call-centres or online channels for enquiries and advice to obtain the right kind of coverage that meets your insurance protection needs at a price acceptable to you.

- Please ensure comparative shopping is done early before your insurance policy expires. Your insurer or takaful operator will advise you at least a month earlier before the expiry of your motor insurance policy.

7. I have just renewed my motor insurance coverage on 1 June 2016. Can I still purchase additional products now to enhance my motor insurance protection?

Yes, you can still purchase additional products to enhance the insurance protection for the same motor vehicle.

Alternatively, you may purchase new motor products that meet your needs, to replace the existing motor insurance coverage for the remaining coverage period. Before terminating your existing motor insurance coverage, please contact your agent, insurer or takaful operator to find out the pro-rated amount of the premium paid which will be refunded to you by your insurer or takaful operator.

Do make informed decisions by shopping around for different quotations by contacting the agents, insurers or takaful operators through their call centres or online channels before you make your purchase.

8. For existing motor insurance policies coverage beyond 1 July 2017, what would be the premium chargeable?

The premiums charged will be based on the policy anniversary date (the date which your motor insurance policy expires) of the motor policy.

9. Will the Motor Third Party insurance product be available for consumers?

Motor Third Party insurance product is still available for consumers who want to purchase basic motor insurance cover at tariff rate.

10. What will happen to my No Claim Discount (NCD)?

The NCD structure will remain unchanged and continue to be transferable from one insurer or takaful operator to another.

You will be entitled to the NCD which you are eligible for.

11. Where can I obtain information of new products available and how do I choose

products that will meet my needs?

You are advised to always check with your insurer or takaful operator or the agent on new products and add-on covers introduced.

Do shop around to make informed purchasing decisions by obtaining different quotations by contacting the agents, insurers or takaful operators through their callcentres or online channels.